Expert Nguyễn Quang Bình provides insights to help readers better understand the risks associated with both methods of coffee export contracts — fixing the price before (“chốt giá trước”) or after (“chốt giá sau”).

Government Recommendation

Table of Contents

One of the most discussed risk-management measures is the recommendation from the Ministry of Agriculture and Rural Development: exporters should avoid signing “differential” contracts (“trừ lùi”) and only sell under “spot” contracts once they already possess the goods.

In coffee exports, both globally and in Vietnam, buyers and sellers often use “differential contracts”, which coexist alongside contracts with fixed prices. In the latter, both parties agree on a specific unit price for the transaction.

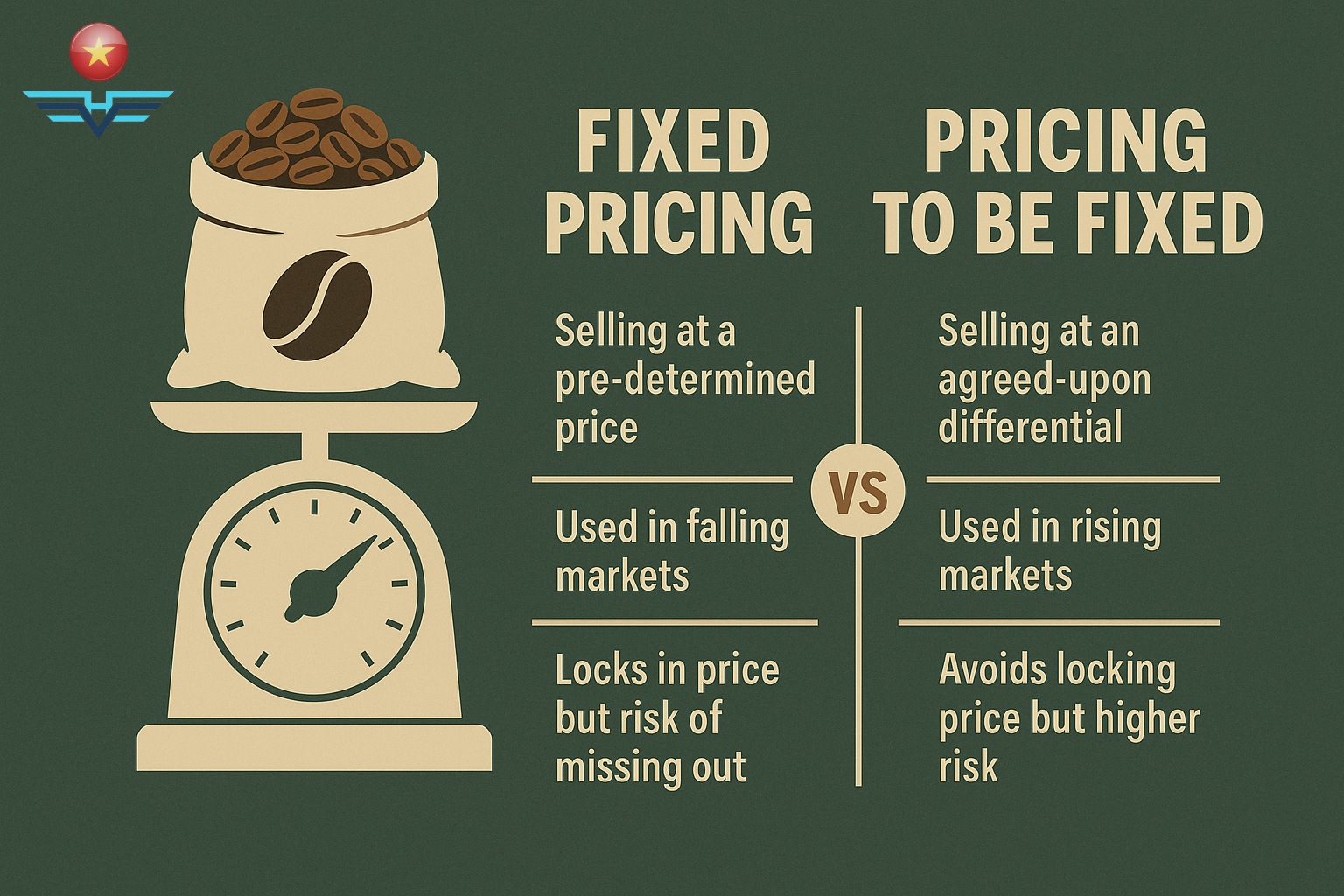

Contracts with a fixed price are known in the trade as “outright contracts” — meaning the price is determined and agreed upon at the time of signing. Although these are still considered forward contracts (based on the London Robusta futures price difference), the key point is that the price is fixed immediately — hence the name “fixed-price” or “price-fixed before” contracts.

Meanwhile, “differential” (or “plus/minus”) contracts are those where the two parties agree on a premium or discount (called differentials) relative to the London Robusta futures price. The final price is only set later, once either side deems it favorable for their buying or selling position.

Fixed Later vs. Fixed Before

This method allows both sides to minimize risk when prices move against their expectations. Such contracts are known as “price-to-be-fixed” (PTBF) contracts — or in Vietnamese, “chốt sau.”

In professional coffee trading:

-

Fixing price before (“chốt trước”) is preferred when prices are trending downward (bear markets).

-

Fixing price later (“chốt sau”) is more advantageous when prices are expected to rise (bull markets).

Sometimes, traders can even infer market direction based on contract types:

-

A surge in “fixed-price” contracts suggests expectations of a market decline.

-

A rise in “price-to-be-fixed” contracts implies hopes for higher prices.

The Ministry’s Warning

Therefore, the Ministry and Vicofa’s warning against “differential” or “price-to-be-fixed” contracts may be understood as their prediction that coffee prices will likely fall this season — though, of course, no one welcomes that outcome.

However, in the previous 2011/12 crop year, Vicofa had issued the same warning — and yet, many exporters faced problems. Banks refused to finance “fixed-price” contracts because prices were too low, leading to potential export losses and unpaid loans. As a result, several exporters defaulted, damaging Vietnam’s coffee reputation abroad.

Some companies, following Vicofa’s advice, sold at fixed prices around $1,900–1,950 per ton, believing those levels were favorable. But soon after, prices kept climbing throughout the season, pushing domestic prices up as well. Unable to buy enough coffee for delivery, many exporters incurred losses or defaulted on shipments.

Thus, the “no-differential-sale” advice proved highly damaging to those who followed it.

An Example

Suppose today an exporter sells at a fixed price of $1,750/ton (a discount of $56 to the January 2012 London price) for December 2011 delivery, assuming prices will fall.

But one week later, the futures price rises to $2,000/ton, lifting local prices correspondingly.

Now the exporter must deliver at $1,750/ton while buying from farmers at $1,950/ton, resulting in losses that could have been avoided with a “chốt sau” contract.

Clearly, the price decline in the current market isn’t caused by too many PTBF contracts being signed.

Market Control and Risk Management

In a market dominated by financial speculators, determining whether to fix prices before or after should be left to enterprises themselves.

They are well aware of how to balance proportions between the two methods to minimize risk exposure.

Despite being one of the world’s largest Robusta exporters, Vietnamese exporters still lack pricing power, making it difficult to stabilize returns for farmers. Strengthening their strategic management will be key for Vietnam to maintain its position as the world’s leading Robusta coffee exporter while improving resilience in volatile markets.