Introduction – The Birth of the Commodity Derivatives Market

Table of Contents

The success achieved through the application of science and technology in agricultural production led to a rapid increase in the supply of agricultural goods. Production not only met domestic demand but also created abundant export opportunities to other regions and countries.

However, due to limited market access, seasonal harvests, and the surge of supply over a short period, producers were often forced into a passive position regarding prices, resulting in significant losses for both suppliers and buyers.

To facilitate the circulation of agricultural commodities, producers and traders began meeting before each harvest season to agree on prices, quantities, quality standards, and delivery dates for future transactions. Initially, these agreements were simple, small-scale, and lacked standardized regulations.

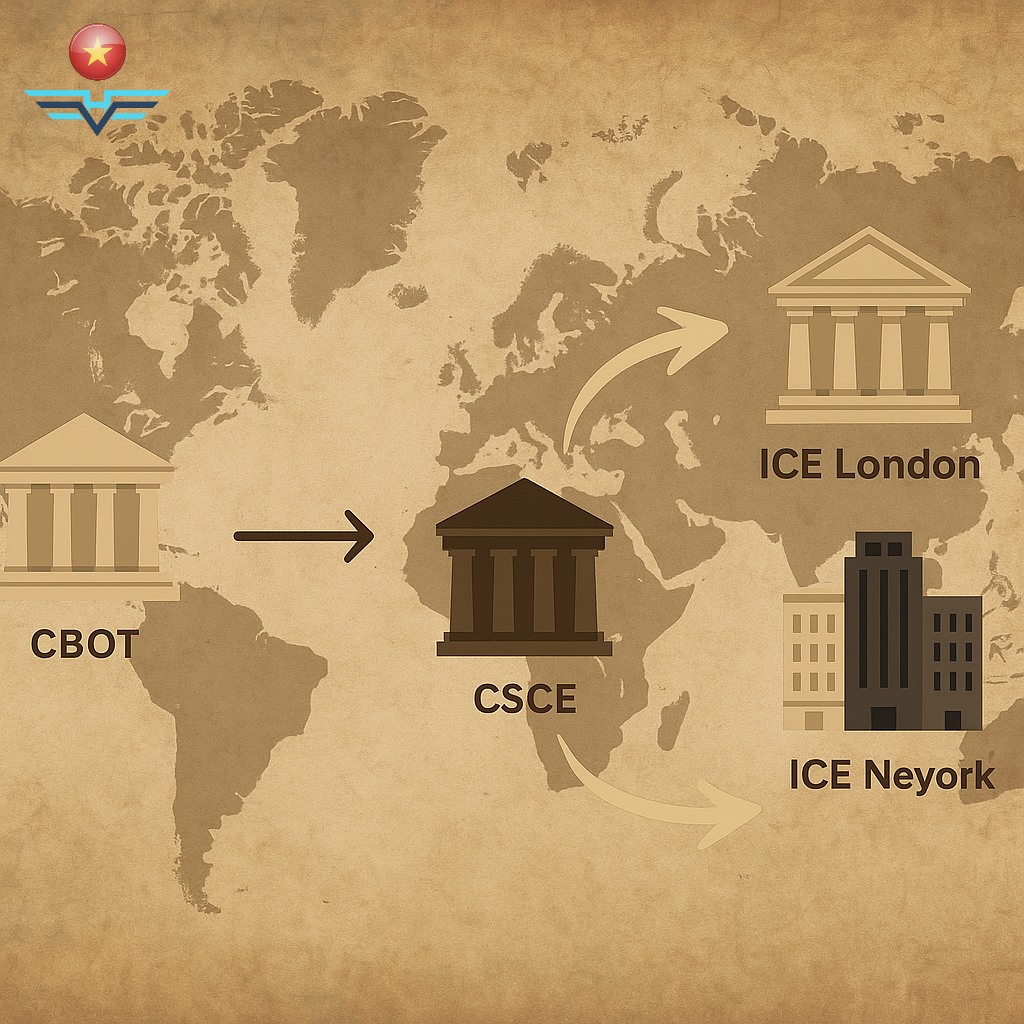

In 1848, the Chicago Board of Trade (CBOT) was established to promote grain trading by standardizing quantity, quality, and developing long-term grain contracts. During its early years, forward contracts were traded. By 1865, CBOT officially introduced standardized contracts, known today as futures contracts.

The emergence of the commodity derivatives market was a natural consequence of a market economy, representing diversification in trade and international free commerce. Derivative products are now applied worldwide, bringing numerous benefits — especially in facilitating the circulation of agricultural goods and reducing risks for producers by transferring price risks to the market.

The First Coffee Derivatives Exchange in the World

The Coffee, Sugar & Cocoa Exchange (CSCE) was the first exchange in the world to trade coffee, sugar, and cocoa futures and options. It was founded in 1882 in New York City as the Coffee Exchange.

-

1914: Sugar futures contracts were introduced.

-

September 28, 1979: The New York Coffee and Sugar Exchange merged with the New York Cocoa Exchange (established in 1925), forming the CSCE.

-

1998: CSCE merged with the New York Cotton Exchange to become a subsidiary of the New York Board of Trade (NYBOT).

The CSCE operated as an independent division under NYBOT, allowing futures and options trading for coffee, sugar, cocoa, and the S&P Commodity Index.

In January 2007, NYBOT merged with the Intercontinental Exchange (ICE) in New York, becoming one of its subsidiaries.

Major International Coffee Derivatives Exchanges

-

Intercontinental Exchange (ICE), New York: Trades primarily Arabica coffee.

-

London International Financial Futures and Options Exchange (LIFFE): Part of the Euronext group, trades mainly Robusta coffee.

-

Brazilian Mercantile and Futures Exchange (BM&F), Brazil.

-

Singapore Commodity Exchange (SICOM), Singapore.

-

Tokyo Grain Exchange (TGE), Japan.

For Arabica coffee, the most actively traded market is ICE New York.

For Robusta coffee, the most active market is LIFFE London.

Prices quoted on these exchanges differ according to the supply and demand of each market.

Principles of Coffee Pricing

When futures contracts reach maturity, the official trading price (FOB – Freight on Board) equals the futures price on the exchange plus or minus a differential — known as the basis differential pricing system.

This differential may reflect:

-

Transportation costs from the exporting to the importing country.

-

Quality discounts and other agreed-upon expenses.

This pricing principle applies to most coffee types worldwide, except for certain specialty coffees.

Example:

For coffee from Kenya, known for its exceptional quality, prices are first determined through a national auction system, and then adjusted in subsequent trades based on the differential pricing principle.

Specifications of ICE Arabica Coffee Futures Contracts

-

Eligible coffee: Washed Arabica produced in Central and South America, Asia, Africa, or unwashed Arabica from Ethiopia.

-

Contract size: 37,500 pounds (≈ 250 bags).

-

Trading hours: 3:30 a.m. – 2:00 p.m. (New York time).

-

In Vietnam: 3:30 p.m. – 2:00 a.m. the next day.

-

-

Price quotation: Cents per pound.

-

Contract months: March, May, July, September, December.

-

Minimum price fluctuation: 0.05 cents/lb = USD 18.75 per contract.

Specifications of ICE Robusta Coffee Futures Contracts

-

Contract size: 10 metric tons.

-

Trading hours: 9:00 a.m. – 5:30 p.m. (London time).

-

In Vietnam: 4:00 p.m. – 12:30 a.m. the next day.

-

-

Price quotation: USD per metric ton.

-

Contract months: January, March, May, July, September, November.

-

Minimum price fluctuation: USD 1/ton = USD 10 per contract.